Compound Interval Finance

Compound Interval Finance: Maximizing Returns with Strategic Stacking

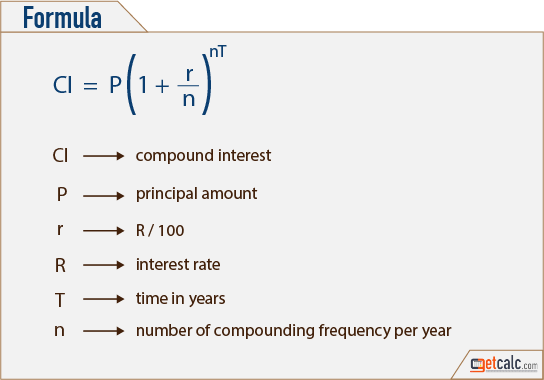

Compound interval finance is a sophisticated investment strategy that leverages the power of compounding interest within defined time intervals to maximize returns. It involves reinvesting earnings—typically interest or dividends—at pre-determined frequencies, allowing the principal to grow exponentially over time. This approach is particularly effective for long-term financial goals such as retirement planning or funding significant future expenses.

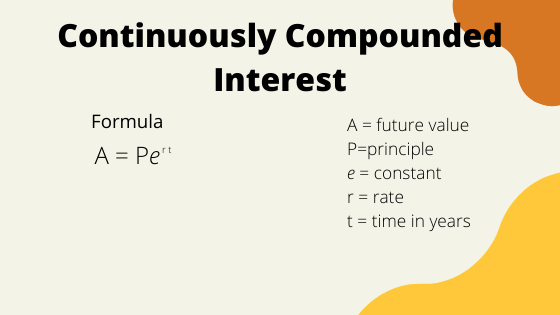

The core principle rests on the 'snowball effect.' Instead of withdrawing earnings, they are added back to the principal. In the next interval, interest is calculated not just on the original investment, but also on the previously earned interest. The more frequently interest is compounded (e.g., daily vs. annually), the faster the overall growth, though the difference diminishes as compounding frequency increases beyond a certain point.

Several key elements define a successful compound interval finance strategy. Firstly, the investment vehicle needs to support regular reinvestment. Common examples include dividend reinvestment plans (DRIPs) for stocks, high-yield savings accounts, certificates of deposit (CDs), and certain bond funds. Selecting the right vehicle depends on risk tolerance, investment horizon, and available capital.

Secondly, the compounding interval is crucial. Shorter intervals lead to faster growth, but might involve more administrative overhead. For example, daily compounding requires frequent monitoring and potential transaction fees. Annually or quarterly compounding may be simpler but less effective for aggressive growth.

Thirdly, contribution strategy plays a significant role. Consistent, periodic contributions, also known as dollar-cost averaging, can smooth out market volatility and enhance long-term returns. Adding to the principal at regular intervals accelerates the compounding process.

Finally, tax implications must be considered. In many jurisdictions, interest and dividend income are taxable, even when reinvested. Understanding these tax obligations is essential for accurate financial planning and to avoid unexpected tax liabilities.

While compound interval finance is powerful, it's not without its caveats. Returns are subject to the performance of the underlying investment. Market downturns can erode accumulated gains. Moreover, the benefits of compounding are most pronounced over long periods. Patience and discipline are essential virtues for successful implementation.

In conclusion, compound interval finance is a potent tool for building wealth over time. By strategically reinvesting earnings at regular intervals, investors can harness the power of compounding to achieve their financial goals. Careful planning, diligent monitoring, and a long-term perspective are key to unlocking its full potential.

920×702 compound intervals complete theory guide from jadebultitude.com

920×702 compound intervals complete theory guide from jadebultitude.com  1024×287 work compound intervals jade bultitude from jadebultitude.com

1024×287 work compound intervals jade bultitude from jadebultitude.com  1140×694 compound finance manage finance from webthat.io

1140×694 compound finance manage finance from webthat.io  544×380 compound interest calculator from getcalc.com

544×380 compound interest calculator from getcalc.com  800×1200 compound interval learn theory theory from www.pinterest.com

800×1200 compound interval learn theory theory from www.pinterest.com  736×1104 compound interval learn theory teaching from www.pinterest.com

736×1104 compound interval learn theory teaching from www.pinterest.com  735×1102 compound interval from www.pinterest.com

735×1102 compound interval from www.pinterest.com  1200×800 compound finance governance attack curve finance founder from coingape.com

1200×800 compound finance governance attack curve finance founder from coingape.com  735×1102 compound interval theory learn theory from www.pinterest.com

735×1102 compound interval theory learn theory from www.pinterest.com  900×900 whats compound interest definition napkin finance answer from napkinfinance.com

900×900 whats compound interest definition napkin finance answer from napkinfinance.com  1920×1080 compound finance work hord explains from www.hord.fi

1920×1080 compound finance work hord explains from www.hord.fi  1280×720 compound finance work from www.cryptoblogs.io

1280×720 compound finance work from www.cryptoblogs.io  1140×532 simple compound intervals digital school from digital-school.net

1140×532 simple compound intervals digital school from digital-school.net  3200×2400 calculate compound interest steps wikihow from wikihow.com

3200×2400 calculate compound interest steps wikihow from wikihow.com  1210×621 continuous compound interest table cruiseero from cruiseero.weebly.com

1210×621 continuous compound interest table cruiseero from cruiseero.weebly.com  1000×563 compound intervals theory diagrams application from www.guitartheorylessons.com

1000×563 compound intervals theory diagrams application from www.guitartheorylessons.com  1200×800 compound intervals theory from hellomusictheory.com

1200×800 compound intervals theory from hellomusictheory.com  608×350 complete guide interval funds work key from www.intellivestwm.com

608×350 complete guide interval funds work key from www.intellivestwm.com  500×286 compound interest national maths from www.national5maths.co.uk

500×286 compound interest national maths from www.national5maths.co.uk :max_bytes(150000):strip_icc()/compoundinterest_final-5c67da5662ba458f8d9d229ab4ca4292.png) 1500×1000 power compound interest calculations examples from www.investopedia.com

1500×1000 power compound interest calculations examples from www.investopedia.com  5292×1771 compound finance from www.orbixtrade.com

5292×1771 compound finance from www.orbixtrade.com :max_bytes(150000):strip_icc()/COMPOUNDINTERESTFINALJPEGcopy-f248781269194135aa6044e088de7af9.jpg) 900×600 compound interest definition from www.investopedia.com

900×600 compound interest definition from www.investopedia.com  560×315 continuous compound interest formula double entry bookkeeping xxx from www.myxxgirl.com

560×315 continuous compound interest formula double entry bookkeeping xxx from www.myxxgirl.com  750×748 compound from ar.inspiredpencil.com

750×748 compound from ar.inspiredpencil.com  1920×717 continuous compound interest formula find cheggcom from www.chegg.com

1920×717 continuous compound interest formula find cheggcom from www.chegg.com  1920×656 solved part continuous compound interest cheggcom from www.chegg.com

1920×656 solved part continuous compound interest cheggcom from www.chegg.com  500×286 visual guide simple compound continuous interest rates from betterexplained.com

500×286 visual guide simple compound continuous interest rates from betterexplained.com