Finance Utility Function

Utility Function in Finance

In finance, a utility function represents an investor's preference for different levels of wealth or consumption. It quantifies the satisfaction or happiness an investor derives from a particular economic outcome, typically expressed in terms of money. The utility function is a cornerstone of modern portfolio theory and plays a vital role in understanding investment decisions and risk aversion.

Key Concepts

- Definition: A utility function, denoted as U(x), assigns a numerical value to each possible outcome (x), reflecting the investor's subjective preference for that outcome. A higher utility value indicates a more preferred outcome.

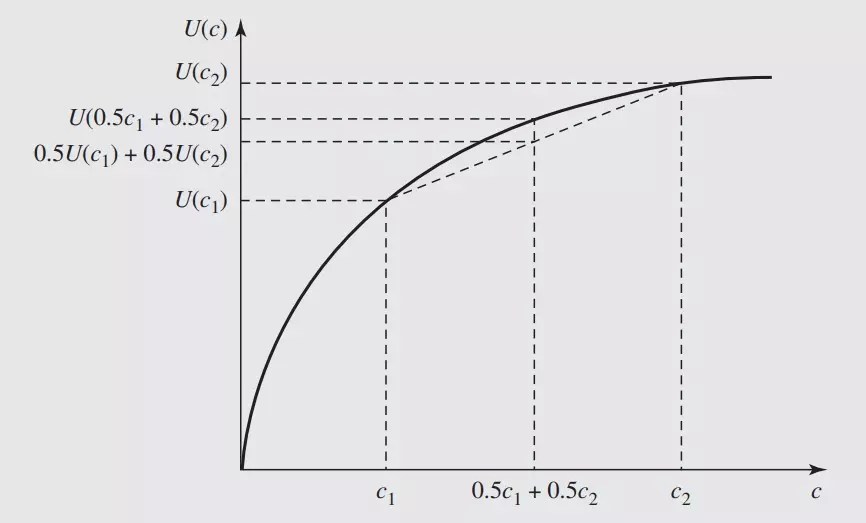

- Risk Aversion: Investors generally exhibit risk aversion, meaning they prefer a certain outcome to a gamble with the same expected value. This is reflected in a concave utility function, where the increase in utility from gaining an additional dollar decreases as wealth increases. This diminishing marginal utility of wealth is a core concept.

- Marginal Utility: Marginal utility is the change in utility resulting from a one-unit change in consumption or wealth. For a risk-averse investor, marginal utility is positive but decreasing.

- Types of Utility Functions: Several functional forms are commonly used, including:

- Logarithmic Utility: U(x) = ln(x). This function exhibits constant relative risk aversion.

- Power Utility: U(x) = xγ / γ, where γ < 1. This allows for varying degrees of risk aversion depending on the value of γ.

- Exponential Utility: U(x) = -e-αx, where α is the coefficient of absolute risk aversion. This function exhibits constant absolute risk aversion.

- Quadratic Utility: U(x) = ax - bx2, where a > 0 and b > 0. This function is simple but has limitations, such as decreasing utility beyond a certain wealth level.

Applications in Finance

- Portfolio Selection: Investors use utility functions to determine the optimal allocation of assets in their portfolio. They seek to maximize their expected utility, balancing risk and return. Different utility functions lead to different optimal portfolios for the same investor.

- Asset Pricing: Utility functions help explain asset prices and risk premiums. Assets that provide higher returns in bad times (when marginal utility is high) will command a lower risk premium than assets that perform poorly in those times.

- Behavioral Finance: Utility functions provide a framework for understanding behavioral biases that influence investment decisions. For example, loss aversion can be modeled by a utility function that is steeper for losses than for gains.

- Decision Making Under Uncertainty: Utility functions are essential for evaluating decisions where outcomes are uncertain. By calculating the expected utility of different choices, investors can make informed decisions that align with their risk preferences.

Limitations

Despite its usefulness, the utility function approach has limitations. Accurately estimating an individual's utility function is challenging, as it's inherently subjective and can change over time. Furthermore, some behavioral biases, such as framing effects, are not easily captured by standard utility functions. The assumption of rationality, which underpins the use of utility functions, may not always hold true in real-world investment scenarios.

In conclusion, the utility function is a powerful tool in finance for representing investor preferences and understanding investment behavior. While acknowledging its limitations, it remains a crucial concept for portfolio management, asset pricing, and analyzing financial decisions under uncertainty.

1024×602 utility function matters works penpoin from penpoin.com

1024×602 utility function matters works penpoin from penpoin.com  1263×694 utility function formula examples graph from www.wallstreetmojo.com

1263×694 utility function formula examples graph from www.wallstreetmojo.com  1500×600 utility finance basics euci from www.euci.com

1500×600 utility finance basics euci from www.euci.com  850×437 structure utility function utility scientific diagram from www.researchgate.net

850×437 structure utility function utility scientific diagram from www.researchgate.net  1024×942 utility function policonomics from policonomics.com

1024×942 utility function policonomics from policonomics.com  866×523 valuing risky cash flows utility theory finance from financestu.com

866×523 valuing risky cash flows utility theory finance from financestu.com  1280×989 utility function asset managment lecture docsity from www.docsity.com

1280×989 utility function asset managment lecture docsity from www.docsity.com  490×351 incorporating utility function decision making process from www.spicelogic.com

490×351 incorporating utility function decision making process from www.spicelogic.com  780×421 illustration utility function scientific diagram from www.researchgate.net

780×421 illustration utility function scientific diagram from www.researchgate.net  850×525 concept utility function scientific diagram from www.researchgate.net

850×525 concept utility function scientific diagram from www.researchgate.net  180×233 utility function practicepdf utility function practice from www.coursehero.com

180×233 utility function practicepdf utility function practice from www.coursehero.com  640×640 typical utility function good scientific diagram from www.researchgate.net

640×640 typical utility function good scientific diagram from www.researchgate.net  850×159 structure utility function scientific diagram from www.researchgate.net

850×159 structure utility function scientific diagram from www.researchgate.net  352×243 diagram utility function scientific diagram from www.researchgate.net

352×243 diagram utility function scientific diagram from www.researchgate.net  616×594 utility function general dsge modeling dynare forum from forum.dynare.org

616×594 utility function general dsge modeling dynare forum from forum.dynare.org  640×640 utility function types scientific diagram from www.researchgate.net

640×640 utility function types scientific diagram from www.researchgate.net  850×584 utility function scientific diagram from www.researchgate.net

850×584 utility function scientific diagram from www.researchgate.net  850×754 scheme utility function scientific diagram from www.researchgate.net

850×754 scheme utility function scientific diagram from www.researchgate.net  690×478 utility function investors wealth scientific diagram from www.researchgate.net

690×478 utility function investors wealth scientific diagram from www.researchgate.net  584×412 forms utility function scientific diagram from www.researchgate.net

584×412 forms utility function scientific diagram from www.researchgate.net  1520×855 digitally transform finance function raconteur from www.raconteur.net

1520×855 digitally transform finance function raconteur from www.raconteur.net  1223×662 solved suppose utility function defined cheggcom from www.chegg.com

1223×662 solved suppose utility function defined cheggcom from www.chegg.com  850×767 utility function describing relation income from www.researchgate.net

850×767 utility function describing relation income from www.researchgate.net