Stratified Sampling Finance

Stratified Sampling in Finance

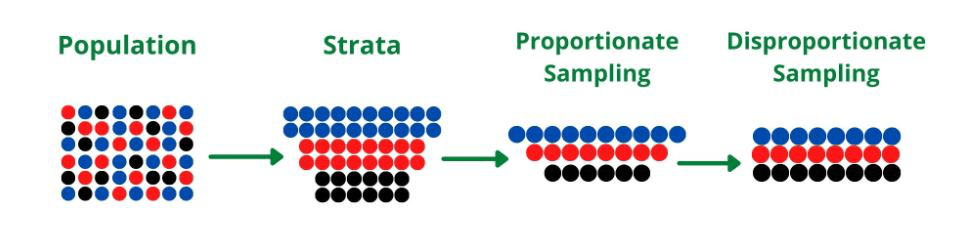

Stratified sampling is a statistical sampling technique widely used in finance to ensure a representative sample is drawn from a population that can be divided into subgroups, or strata. These strata are created based on shared characteristics that are relevant to the financial analysis being conducted.

Why Use Stratified Sampling in Finance?

The primary reason for using stratified sampling is to improve the accuracy and reliability of the sample. In finance, populations are often heterogeneous. For example, a portfolio might contain assets with vastly different market capitalizations, risk profiles, or industry classifications. Using simple random sampling could lead to an under- or over-representation of certain groups, potentially skewing the results of any analysis performed on the sample. Stratified sampling mitigates this risk by guaranteeing that each stratum is adequately represented in the final sample.

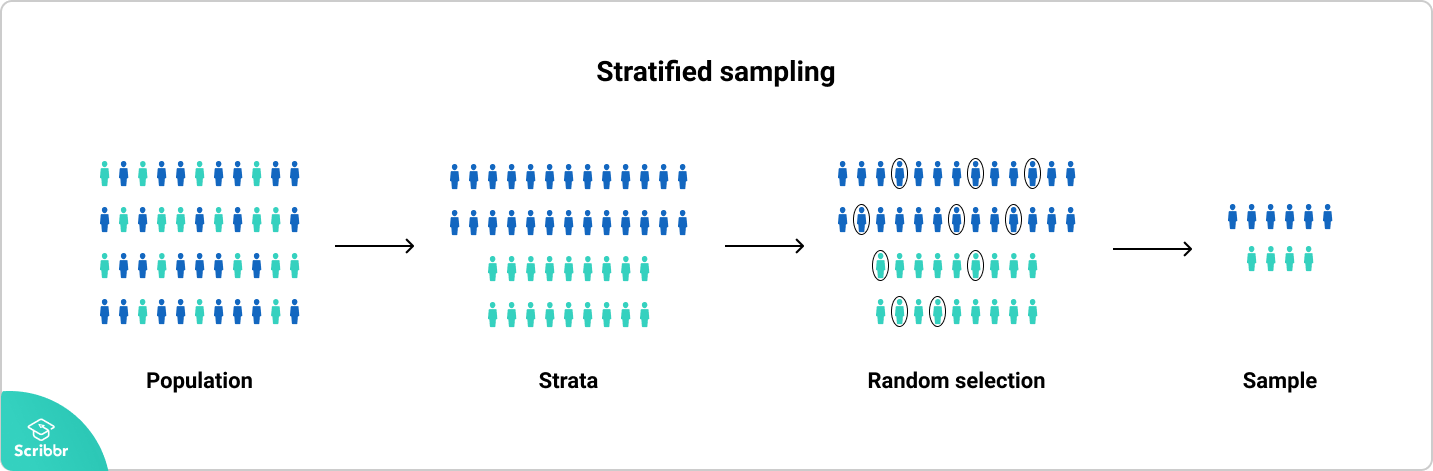

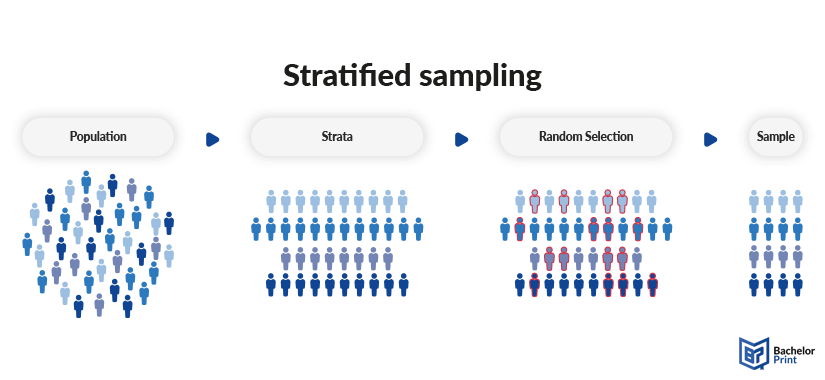

How Stratified Sampling Works

The process involves several key steps:

- Identify Relevant Strata: Determine the characteristics that are most relevant to the analysis. Examples include market capitalization (large-cap, mid-cap, small-cap), industry sector (technology, healthcare, finance), or credit rating (AAA, AA, A, BBB).

- Divide the Population: Segment the entire population into distinct strata based on the chosen characteristics. Each element should belong to only one stratum.

- Determine Sample Size within Each Stratum: Decide on the number of elements to sample from each stratum. This can be done proportionally (where the sample size for each stratum is proportional to its size in the population) or disproportionally (where certain strata are oversampled or undersampled based on the specific goals of the analysis). For example, if a small stratum is considered particularly important, it might be oversampled.

- Randomly Sample from Each Stratum: Use simple random sampling (or another appropriate random sampling method) to select the required number of elements from each stratum.

- Combine the Samples: Combine the samples from all strata to create the final stratified sample.

Examples in Finance

- Portfolio Analysis: When analyzing a large investment portfolio, stratified sampling can ensure adequate representation of different asset classes (stocks, bonds, real estate), sectors, or geographic regions.

- Credit Risk Assessment: When evaluating a loan portfolio, stratifying borrowers by credit score or loan size can provide a more accurate assessment of overall credit risk.

- Market Research: When surveying investors about their investment preferences, stratifying by age, income level, or investment experience can provide a more nuanced understanding of the market.

- Auditing: When auditing financial statements, stratifying transactions by size can help auditors focus on the most material transactions and ensure a representative sample across different transaction categories.

Advantages and Disadvantages

Advantages:

- Improved accuracy and representativeness of the sample.

- Reduced sampling error compared to simple random sampling.

- Ability to analyze individual strata separately.

Disadvantages:

- Requires knowledge of the population and the ability to divide it into strata.

- Can be more complex and time-consuming than simple random sampling.

- If the strata are poorly defined, the benefits of stratified sampling may be diminished.

In conclusion, stratified sampling is a valuable tool for financial professionals who need to obtain representative samples from heterogeneous populations. By carefully defining strata and appropriately allocating sample sizes, analysts can improve the accuracy and reliability of their analyses, leading to better informed decisions.

422×257 stratified sampling breaking finance from breakingdownfinance.com

422×257 stratified sampling breaking finance from breakingdownfinance.com  994×599 stratified sampling statsig docs from docs.statsig.com

994×599 stratified sampling statsig docs from docs.statsig.com  400×326 stratified sampling statcalculatorscom from statcalculators.com

400×326 stratified sampling statcalculatorscom from statcalculators.com  638×479 stratified sampling from www.slideshare.net

638×479 stratified sampling from www.slideshare.net  1568×496 stratified sampling eco easy from ecoiseasy.com

1568×496 stratified sampling eco easy from ecoiseasy.com  752×435 stratified sampling introduction examples built from builtin.com

752×435 stratified sampling introduction examples built from builtin.com  1101×429 stratified sampling definition guide examples from www.scribbr.com

1101×429 stratified sampling definition guide examples from www.scribbr.com  1200×675 stratified sampling examples types differences from www.examples.com

1200×675 stratified sampling examples types differences from www.examples.com  1200×600 introducing stratified sampling from www.statsig.com

1200×600 introducing stratified sampling from www.statsig.com  870×652 stratified sampling teaching resources from www.tes.com

870×652 stratified sampling teaching resources from www.tes.com  1433×471 stratified sampling step step guide examples from www.scribbr.com

1433×471 stratified sampling step step guide examples from www.scribbr.com  1103×561 stratified random sampling overview proscons from corporatefinanceinstitute.com

1103×561 stratified random sampling overview proscons from corporatefinanceinstitute.com  1024×768 stratified sampling powerpoint id from www.slideserve.com

1024×768 stratified sampling powerpoint id from www.slideserve.com  463×280 stratified sampling definition formula calculation from www.wallstreetmojo.com

463×280 stratified sampling definition formula calculation from www.wallstreetmojo.com  630×548 stratified sampling definition advantages examples statistics jim from statisticsbyjim.com

630×548 stratified sampling definition advantages examples statistics jim from statisticsbyjim.com  825×380 stratified sampling definition guide from www.bachelorprint.com

825×380 stratified sampling definition guide from www.bachelorprint.com  685×383 stratified sampling method definition formula examples from www.wallstreetmojo.com

685×383 stratified sampling method definition formula examples from www.wallstreetmojo.com  650×450 stratified sampling easy quick step step guide from www.bachelorprint.com

650×450 stratified sampling easy quick step step guide from www.bachelorprint.com  960×233 stratified sampling pandas geeksforgeeks from www.geeksforgeeks.org

960×233 stratified sampling pandas geeksforgeeks from www.geeksforgeeks.org  640×480 stratified sampling machine learning reasontown from reason.town

640×480 stratified sampling machine learning reasontown from reason.town  1920×1080 stratified sampling stratified random sampling definition method from fity.club

1920×1080 stratified sampling stratified random sampling definition method from fity.club