Binomial Finance

Here's an HTML rendition explaining binomial finance in about 500 words:

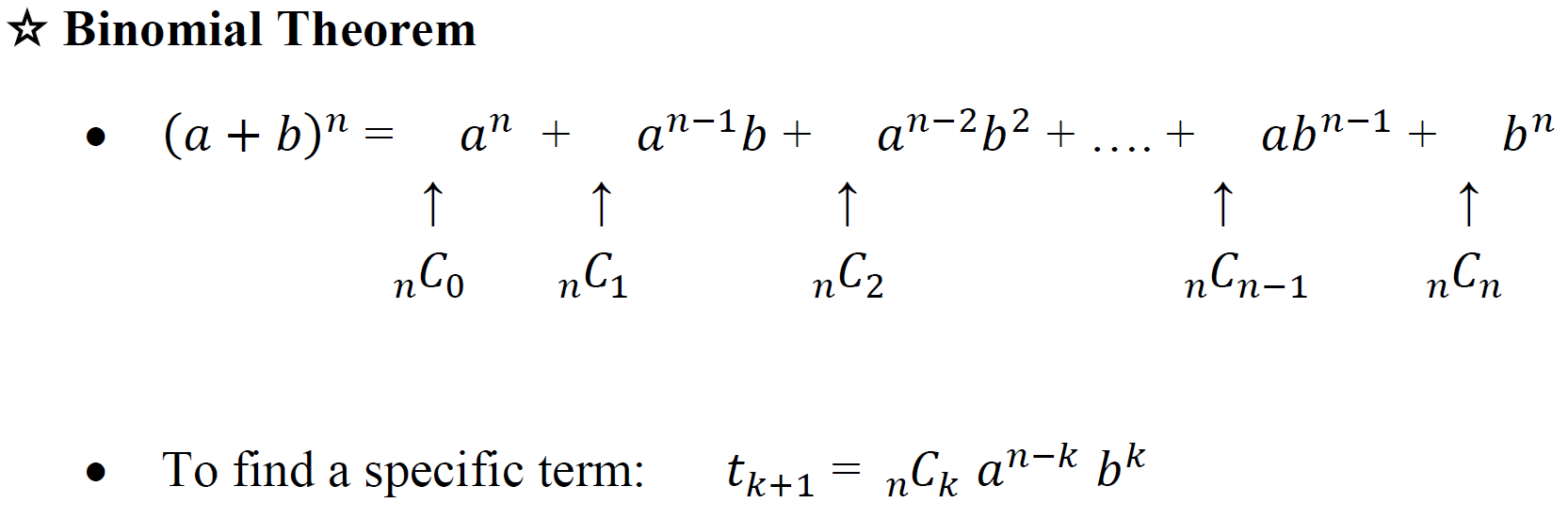

Binomial Option Pricing Model

The Binomial Option Pricing Model (BOPM) is a popular method for valuing options. Unlike the Black-Scholes model, which relies on a continuous-time stochastic process, the BOPM uses a discrete-time model, making it conceptually simpler and more versatile. It's particularly useful for valuing options with complex features or when underlying asset returns don't perfectly fit a log-normal distribution.

Core Concepts

The model works by constructing a binomial tree representing the possible paths of the underlying asset's price over the option's life. At each node in the tree, the price can either go "up" or "down" by a certain factor. These factors are determined by volatility and time to expiration. The key is to create a risk-free portfolio at each node, comprising the option and the underlying asset, that guarantees the same payoff regardless of whether the price goes up or down.

The model rests on a few key assumptions:

- The price of the underlying asset follows a binomial distribution.

- There are only two possible prices for the underlying asset at each time step.

- A risk-free interest rate is constant and known over the option's life.

- No arbitrage opportunities exist.

- The market is frictionless (no transaction costs or taxes).

How it Works

- Build the Binomial Tree: Start with the current price of the underlying asset. For each time step, calculate the possible "up" and "down" prices. The size of the "up" (u) and "down" (d) factors are derived from the volatility and the time step.

- Calculate Option Values at Expiration: At the final nodes of the tree (expiration date), the option's value is simply its intrinsic value. For a call option, this is max(0, Stock Price - Strike Price). For a put option, it's max(0, Strike Price - Stock Price).

- Work Backwards Through the Tree: This is the crucial step. At each node before expiration, calculate the option's value using the risk-neutral probability of an upward movement (p). This probability is derived from the risk-free interest rate, the "up" factor, and the "down" factor. The formula to compute option value (C) is : C = [p * C_up + (1-p) * C_down] / (1 + r), where C_up and C_down are the option values at the next time step in the up and down states, respectively, and 'r' is the risk-free rate.

- Value at the Root Node: The option value at the very beginning (root node) of the tree is the theoretical fair value of the option.

Advantages

- Intuitive and Easy to Understand: The step-by-step construction and backward induction are relatively straightforward.

- Handles Complex Options: The BOPM can accommodate American-style options (exercisable at any time before expiration) and options with dividends more easily than the Black-Scholes model. Early exercise can be incorporated by checking at each node whether the immediate exercise value is greater than the calculated value.

- Flexibility: It can be adapted to various underlying asset price processes.

Disadvantages

- Computational Intensity: As the number of time steps increases for greater accuracy, the computational complexity grows.

- Assumptions: The model still relies on simplifying assumptions. The constant volatility and interest rate assumptions may not hold in real-world markets.

- Convergence: While increasing the number of steps improves accuracy, the model converges to the Black-Scholes value as the number of steps approaches infinity *if* the parameters are calibrated consistently.

Conclusion

The Binomial Option Pricing Model is a valuable tool for understanding and valuing options, particularly when dealing with American-style options or when the assumptions of the Black-Scholes model are not met. Its intuitive nature and flexibility make it a staple in finance education and practice. While it has limitations, it provides a robust framework for option pricing.

1427×814 binomial from chrispiech.github.io

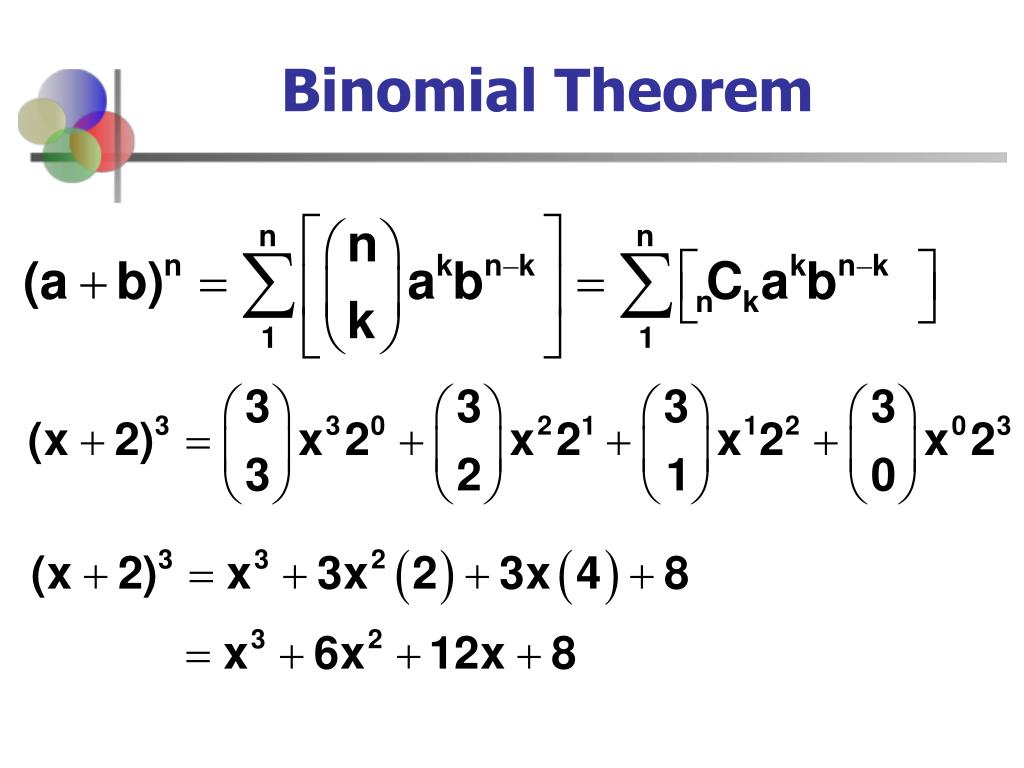

1427×814 binomial from chrispiech.github.io  1024×768 binomial probability distribution powerpoint from www.slideserve.com

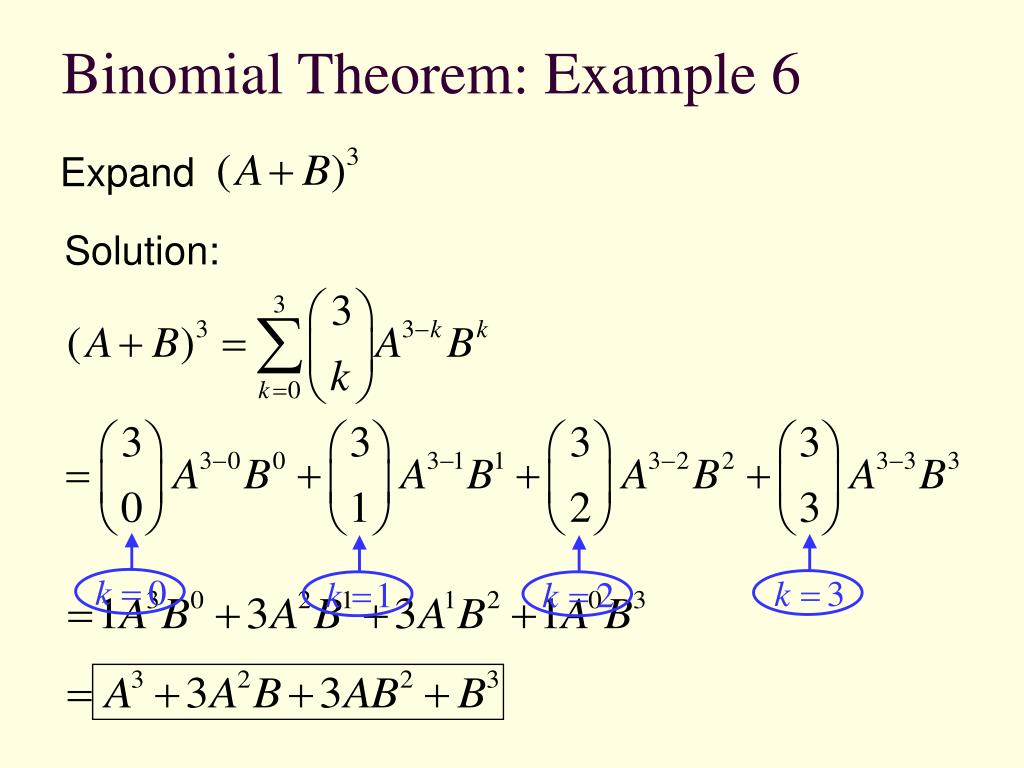

1024×768 binomial probability distribution powerpoint from www.slideserve.com  474×355 binomial theorem powerpoint id from www.slideserve.com

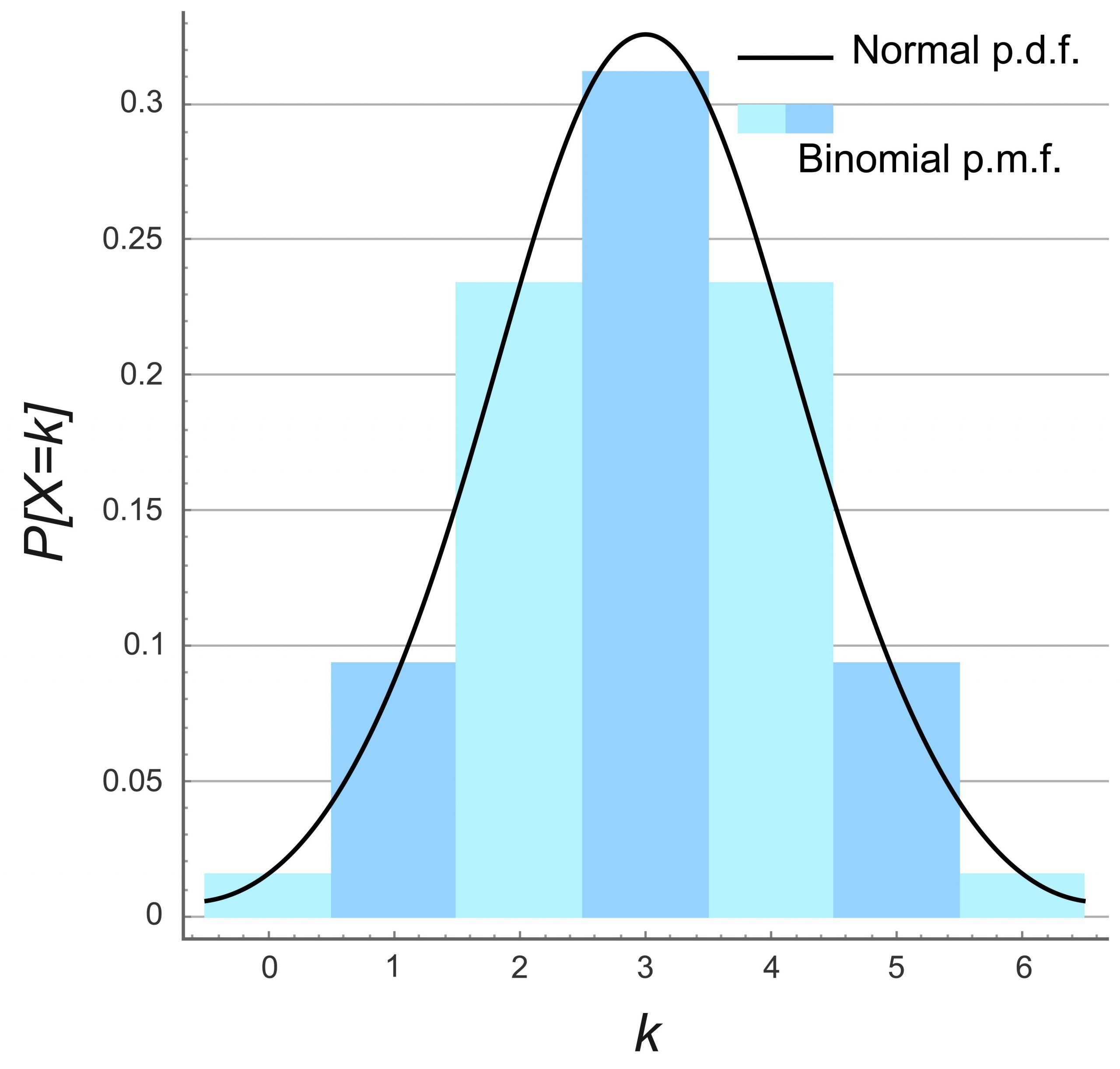

474×355 binomial theorem powerpoint id from www.slideserve.com  2560×2443 binomial probability distribution data science learning keystone from datasciencelk.com

2560×2443 binomial probability distribution data science learning keystone from datasciencelk.com  1280×720 binomial series expand function surefire examples from calcworkshop.com

1280×720 binomial series expand function surefire examples from calcworkshop.com  1800×900 binomial theorem explanation examples from www.storyofmathematics.com

1800×900 binomial theorem explanation examples from www.storyofmathematics.com  0 x 0 binomial distribution fully explained examples from calcworkshop.com

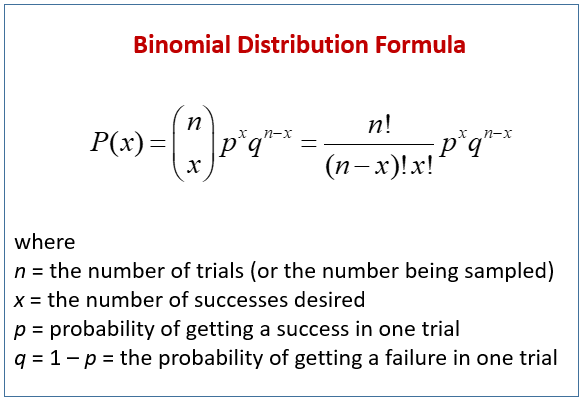

0 x 0 binomial distribution fully explained examples from calcworkshop.com  584×403 binomial distribution examples solutions formulas from www.onlinemathlearning.com

584×403 binomial distribution examples solutions formulas from www.onlinemathlearning.com  1024×461 binomial distribution definition probability calculate negative from www.wallstreetmojo.com

1024×461 binomial distribution definition probability calculate negative from www.wallstreetmojo.com  507×352 binomial series examples solutions from www.onlinemathlearning.com

507×352 binomial series examples solutions from www.onlinemathlearning.com  1024×768 binomial distribution powerpoint from www.slideserve.com

1024×768 binomial distribution powerpoint from www.slideserve.com  406×185 binomial definition illustrated mathematics dictionary from www.mathsisfun.com

406×185 binomial definition illustrated mathematics dictionary from www.mathsisfun.com  1200×600 binomial theorem definition formula proof examples from www.adda247.com

1200×600 binomial theorem definition formula proof examples from www.adda247.com  625×407 binomial distribution definition properties calculation formula from www.cuemath.com

625×407 binomial distribution definition properties calculation formula from www.cuemath.com  674×274 finding terms binomial expansion examples solutions worksheets from www.onlinemathlearning.com

674×274 finding terms binomial expansion examples solutions worksheets from www.onlinemathlearning.com  2560×1920 binomial coefficient from aussiemathematician.io

2560×1920 binomial coefficient from aussiemathematician.io  1024×561 definition binomial math definitions letter from www.subjectcoach.com

1024×561 definition binomial math definitions letter from www.subjectcoach.com  1000×500 binomial distribution business statistics definition formula from www.geeksforgeeks.org

1000×500 binomial distribution business statistics definition formula from www.geeksforgeeks.org  441×215 binomial theorem study material iit jee askiitians from www.askiitians.com

441×215 binomial theorem study material iit jee askiitians from www.askiitians.com  1024×577 binomial expansion examples solutions agnes hendricks blog from storage.googleapis.com

1024×577 binomial expansion examples solutions agnes hendricks blog from storage.googleapis.com  561×361 binomial theorem geeksforgeeks from www.geeksforgeeks.org

561×361 binomial theorem geeksforgeeks from www.geeksforgeeks.org  700×412 binomial definition binomial from www.worksheetsplanet.com

700×412 binomial definition binomial from www.worksheetsplanet.com  740×266 binomial theorem examples solutions examples worksheets from www.onlinemathlearning.com

740×266 binomial theorem examples solutions examples worksheets from www.onlinemathlearning.com  1280×720 binomial distribution youtube from www.youtube.com

1280×720 binomial distribution youtube from www.youtube.com  1000×600 binomial theorem proof math village from mathvilage.blogspot.com

1000×600 binomial theorem proof math village from mathvilage.blogspot.com  1513×877 binomial distribution quality gurus from www.qualitygurus.com

1513×877 binomial distribution quality gurus from www.qualitygurus.com  750×356 binomial expansion formula examples solutions worksheets from www.onlinemathlearning.com

750×356 binomial expansion formula examples solutions worksheets from www.onlinemathlearning.com  600×280 phys binomial theorem from www.physics.udel.edu

600×280 phys binomial theorem from www.physics.udel.edu  1024×526 binomial distribution formula calculator excel template from www.educba.com

1024×526 binomial distribution formula calculator excel template from www.educba.com  1024×768 binomial theorem from studylib.net

1024×768 binomial theorem from studylib.net  1920×1080 lesson video binomial theorem nagwa from www.nagwa.com

1920×1080 lesson video binomial theorem nagwa from www.nagwa.com  0 x 0 prove binomial theorem induction youtube from www.youtube.com

0 x 0 prove binomial theorem induction youtube from www.youtube.com  1536×864 binomial nomenclature definition examples biology dictionary from www.biologyonline.com

1536×864 binomial nomenclature definition examples biology dictionary from www.biologyonline.com  930×390 binomial expansion cie math solutions from ciemathsolutions.blogspot.com

930×390 binomial expansion cie math solutions from ciemathsolutions.blogspot.com  436×470 distribucion binomial formula ejemplos from elprofe.online

436×470 distribucion binomial formula ejemplos from elprofe.online :max_bytes(150000):strip_icc()/dotdash_v3_Understanding_the_Binomial_Option_Pricing_Model_Nov_2020-05-db5a8f5280ef404b8e2411bd063beef9.jpg) 6009×3959 understanding binomial option pricing model from www.investopedia.com

6009×3959 understanding binomial option pricing model from www.investopedia.com  1049×571 definition binomial nomenclature rules examples from www.ahmadcoaching.com

1049×571 definition binomial nomenclature rules examples from www.ahmadcoaching.com  1024×572 binomial theorem expand binomial express result from www.numerade.com

1024×572 binomial theorem expand binomial express result from www.numerade.com  1024×974 understanding shape binomial distribution from www.statology.org

1024×974 understanding shape binomial distribution from www.statology.org  750×511 general middle terms binomial expansion formulas examples from byjus.com

750×511 general middle terms binomial expansion formulas examples from byjus.com  1640×1087 read binomial distribution table from www.statology.org

1640×1087 read binomial distribution table from www.statology.org  1280×1920 demystifying binomial distribution dennis robert from towardsdatascience.com

1280×1920 demystifying binomial distribution dennis robert from towardsdatascience.com  1024×630 overview binomial nomenclature rules from eduinput.com

1024×630 overview binomial nomenclature rules from eduinput.com  750×618 binomial nomenclature rules binomial nomenclature from byjus.com

750×618 binomial nomenclature rules binomial nomenclature from byjus.com  1665×551 binomial theorem studypug from www.studypug.com

1665×551 binomial theorem studypug from www.studypug.com  773×247 binomial expansion cureece from cureece.blogspot.com

773×247 binomial expansion cureece from cureece.blogspot.com  1024×768 binomial distribution examples dbinom pbinom qbinom rbinom from statisticsglobe.com

1024×768 binomial distribution examples dbinom pbinom qbinom rbinom from statisticsglobe.com  1747×914 binomial theorem formula formula maths from formulainmaths.in

1747×914 binomial theorem formula formula maths from formulainmaths.in  1024×646 binomial theorem toppers bulletin from www.toppersbulletin.com

1024×646 binomial theorem toppers bulletin from www.toppersbulletin.com  1024×768 binomial probability formula statistics theprobability from theprobability.netlify.app

1024×768 binomial probability formula statistics theprobability from theprobability.netlify.app